- Stocks and Income by Alts

- Posts

- Institutional-Grade Options from Swaggy

Welcome Institutional-Grade Options by Benedict Maynard.

Brought to you by your friends with benefits at Stocks & Income.

What’s Institutional-Grade Options?

We’ve recruited Benedict Maynard, the guy who literally wrote the book on options trade, to produce a fortnightly newsletter that shows you how to trade options intelligently.

No stupid scams. No naked shorts. He’s going to teach you the techniques he refined over 20 years on the trading desk in London.

Each issue will focus on a specific investment thesis and then show you how to build a trade around it.

What’s today’s idea?

Let’s begin with a quote from CNBC this week:

“The market is priced to perfection right now, I mean, we just hit all-time highs today,” Cheryl Young, private advisor at the Rockefeller Global Family Office, said on CNBC’s “Closing Bell” on Monday. “So, any shocks could cause some pretty big pullbacks here. So, I still love most of these Magnificent Seven names, but I’m adding protection right now.”

Put another way, the prices of high-growth, large-cap stocks have reached extremes relative to more value-oriented large-cap stocks.

This is shown by the difference between the Russell 1000 Growth Index ($IWF) and the Russell 1000 Value Index ($IWD) over the last several years.

Growth stocks are at extreme valuations relative to value stocks as investors have gone all in on the tech story and eschewed much else.

This can be seen by plotting a ratio between the Russell 1000 Growth (RLG) and the Russell 1000 Value (RLV) indices, which is simply the RLG divided by RLV.

Current levels are in excess of the Dot-Com bubble that burst at the turn of this century. The chart has also created a triple-top formation, which tends to indicate a reversal.

As alluded to earlier, reversals from Growth to Value dominance are not gentle affairs. The peak that formed the Dot-Com bubble reversed swiftly, decimated portfolios, and ushered in a multi-year dominance of value investing, which lasted until the middle of 2006.

The sell-off that occurred in 2022 was the most recent and very swift decline. Today, we are back to the extreme.

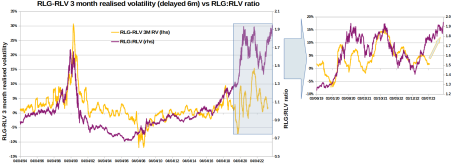

Moreover, there is a close relationship between the RLG:RLV ratio and the volatility that Growth exhibits in excess of Value (chart above).

What's in each index?

The Russell 1000 Growth Index is dominated by tech companies.

The Russell 1000 Value Index is more evenly distributed and contains lots of household names that you know and/or love.

The indices were constructed in the late 1970s, so there is a nearly 45-year trading history.

The dominance of one index over the other has alternated frequently, but they've always reverted to each other.

You can see that the growth index is significantly overvalued today compared to historic norms.

Potential Returns

The trade uses six-month options, and the outlay is relatively small.

Despite the small initial outlay, the magnitude of previous reversals has created very large returns in the past. The average return since 2020 (when the valuation discrepancy was not even as stretched as it is now) would have created an excess of a 15x profit using today’s option prices when a reversal has occurred - i.e., turning $500 into $7,500.

Since 2020, when a reversal didn’t happen, only the premium has been lost - i.e. your $500 bet.

The Strategy

By construction, Growth and Value factors target opposite and opposing fundamental stock attributes, and IWF and IWD do this within the confines of the 1000 largest US stocks.

Our trade is a put switch, which involves buying a put option on one instrument and selling (or shorting) a put option on another instrument - in this case, buying a put option on iShares Russell Growth ETF (IWF) and selling a put on iShares Russell Value ETF (IWD).

Both put options have

That’s all for today. Special thanks to Benedict Maynard for this.

Make sure to subscribe if you want more like this.

Cheers,

Wyatt